THE ECONOMIC DEATH SPRIAL HAS BEEN TRIGGERED

Gordon T. Long

One of the strategies is the Asian Mercantile Strategy. The other is the US Dollar Reserve Currency Strategy.

These two strategies have worked in harmony because they fed off each other, each reinforcing the other. However, today the realities of debt saturation have brought the virtuous spiral to an end.

One of the two global strategies enabled the Asian Tigers to emerge and grow to the extent that they are now the manufacturing and potentially future economic engine of the world.

The other allowed the US to live far beyond its means with massive fiscal deficits, chronic trade imbalances and more recently, current account imbalances. The US during this period has gone from being the richest country on the face of the globe to the biggest debtor nation in the world.

First we need to explore each strategy, how they worked symbiotically, what has changed and then why the virtuous cycle is now accelerating into a vicious downward spiral.

ASIAN MERCANTILE STRATEGY

The Asian Mercantile Strategy started with the emergence of Japan in the early 1980s, expanded with the Asian Tigers in the 90s and then strategically dominated with China in the first decade of this century.

Initially, Japan's products were poor quality and limited to cheap consumer products. Japan as a nation had neither the raw materials, capital markets, nor domestic consumption market to compete with the giant size of the USA.

To compensate for its disadvantages, Japan strategically targeted its manufacturing resources for the US market. By doing this, the resource poor island nation took the first step in becoming an export economy - an economy centered on growth through exports versus an economy like the US, where an excessive 70% of GDP is dependent on domestic consumption.

The strategy began to work as Japan took full advantage of its labor differential that was critical in the low end consumer product segment, which it initially targeted. Gradually, as capital availability expanded, Japan broadened its manufacturing scope, moving into higher levels of consumption products requiring higher levels of quality and achieving brand recognition.

Success soon became a problem as the Yen began to strengthen. To combat this the Japanese implemented the second critical component of what became the Asian Mercantile Strategy template. It began to manipulate its currency by aggressively intervening in the forex market to keep the yen weak.

Further success forced Japan to move to a more aggressive forex strategy to maintain a currency advantage. It was strategically decided that Japan's large and growing foreign reserves were to be re-invested back into the US. By buying US Agency and US Treasury debt instruments it kept the dollar strong relative to the Yen. The more successful Japan became, the more critical this strategy became. In the 80s Japan dominated global expansion as it brought US automotive and consumer electronics' manufacturing to its knees.

By the early 90s the Japanese labor advantage was quickly being lost to the Asian Tigers because the Yen versus the Asian Tiger currencies was too strong. The Asian Tigers were following the Japanese model. The Asian Crisis in 1997 re-enforced to all Asian players the importance of holding large US dollar denominated reserves. This further accelerated and reinforced the strategy of purchasing US Treasury and Agency debt.

With China's acceptance into the World Trade Organization (WTO), China emerged on the scene in full force. Armed with the lessons of the last twenty years, China took the Asian Mercantile Strategy to another level in its ongoing evolution.

The results were one of the largest and fastest transfers of industrial power ever to occur in history. In ten years, China assumed the role of the world's undisputed industrial powerhouse in the world.

The virtuous cycle further accelerated as Asia became more dominant because its reserves, reinvested back in the US, began to have a larger and larger impact. The more Asia bought US Treasury and Agency debt, the lower US interest rates were forced, allowing Americans to finance more and more consumption. The more Asia bought US securities, the stronger the US dollar was against Asian currencies, and therefore the cheaper Asian products were relative to US manufactured products. It was a self reinforcing Virtuous Cycle.

The result was a staggering 46,000 factories transferred from the US to Asia over the same 10 year period. The transfer set the stage for chronic unemployment and public funding problems, but it was temporarily hidden by equally massive increases in debt spending.

The low interest rate driven housing bubble, being of historic proportions, made Americans feel richer than they were. They took on excess debt in various forms such as Home Equity Loans (HELOCs) at unprecedented levels. The acceleration of debt materially impacted both the GDP and employment of the nation through Real Estate, Construction and Mortgage Finance job growth further hiding underlying problems.

US DOLLAR RESERVE CURRENCY STRATEGY

Since President Richard Nixon took the US off the Gold Standard in 1971, the US has adopted what I refer to as the US Dollar Reserve Strategy. After the Second World War, at the Bretton Woods Conference, the US dollar was accepted as the world's reserve currency and as such was pegged to Gold at a fixed rate of $35/oz. due to massive Vietnam war costs and President Johnson Great Society, the US could no longer honor its agreement. In 1971, when France demanded conversion payment in Gold, the US refused. At this point the US become a fiat currency, not backed by anything other than the full faith and credit of Washington politicos.

What were other countries to do in retaliation? What quickly became evident was there was little they could do. The fact was that international trade was conducted in US dollars as a matter of necessity due to the dominance of US export trade; and as such, nations were forced to have US dollars to transact international trade.

Additionally, the US established agreements with oil producing Middle East countries that oil could only be sold in US dollars. Since energy is a dominant import cost for most nations, this secured the strategic position and requirement that the US dollar would be maintained as the preeminent reserve currency by trading nations.

What this strategy meant to the US was that it could now print money, and effectively export the potential inflationary consequences of its actions. The 1970s were initially marked by dramatic increases in US inflation as the strategy took hold and was implemented. By the time of President Reagan's presidency, the strategy was working thanks to some herculean efforts by Chairman Volker at the Federal Reserve. This well executed strategy is what I refer to as the US Reserve Currency Strategy.

The strategy allowed Regan to implement 'Reaganomics' and his new Supply Side economic policies which launched the longest bull market in US history. Further enhanced by an extremely loose monetary policy under Greenspan, relaxed reserve requirements under Clinton, and tax cuts under George Bush II, the US moved quickly from being the world's richest country to being the world's largest debtor.

market in US history. Further enhanced by an extremely loose monetary policy under Greenspan, relaxed reserve requirements under Clinton, and tax cuts under George Bush II, the US moved quickly from being the world's richest country to being the world's largest debtor.

Historic debt growth was built up without the disease of inflation infecting the US economy. This is explained by inflation that was effectively exported whenever increasing levels of US dollars were printed by the US Treasury.

Any threat to this strategy was rapidly challenged by US military power. As an example, when Saddam Hussein, President of Iraq, decided to sell Iraq oil denominated in Euros, he was invaded by US forces three months later and removed from power. When Libyan leader Muammar Gaddafi wanted gold in exchange for Libyan oil, he almost immediately found himself the target of US planned military intervention.

Presently, oil is still sold only in US dollars, but more and more trade deals are being negotiated between China and its trading partners. This is a serious threat to the US and the US Dollar Reserve Strategy.

THE SYMBIOTIC RELATIONSHIP

One of the reasons the US Reserve Strategy has worked for as long as it has, is because there was an incentive by other countries to sterilize the US dollars they received. This, in the case of Asia, was because of the Asian Mercantile Strategy they were executing. By sterilizing US dollars, they held down their currency's exchange rate, which helped their exports though creating potential domestic inflation. Until recently, these inflation pressures have been manageable.

In the case of Europe, the Euro was only coming into existence in the late 90s, but then quickly moved from well below par to nearly 1.50 to the US dollar, causing competitive problems for European export trade for many peripheral countries (PIIGS).

The Asian Export Strategy and the US Reserve Dollar Strategy were symbiotic for a number of reasons:

1. Though the Asian Export Strategy was an Export Trade Imbalance game and the US Dollar Reserve Strategy a Volume Trade game, both were centered on global trade. The US won by increased global trading and the growing requirement for the US dollars it required - dollars that could be increased to pay for the military industrial complex without increasing taxation and used as reserves for global banking growth. Asia won by getting an ever increasing share of a growing volume of trade.

2. The US as a 70% consumption economy needed cheap financing to sustain its insatiable consumption. Asia needed consumption to absorb its growing exports.

3. The US needed a strong dollar to attract financing for its debt. Asia saw US debt as a store for its growing reserves that additionally reduced financing costs for its export products. In a way Asia was offering a form of vendor financing or 'lay away' financing.

4. US corporations saw 'off-shoring', 'outsourcing' and 'rightsizing' as major productivity improvements. The Asian Mercantile Strategy offered American corporations an opportunity to significantly increase profitability while Asia needed every increasing and larger market segments to penetrate. US corporations brought know-how, branding and capital to the Asian economies who desperately needed these strengths to employ unskilled populations, increase standards of living and reduce the always present and potential social unrest.

5. The US economy which had shifted from an industrial economy to a services economy was quickly becoming a financial economy with 44% of the stock market being financials. The financial economy needed increasing capital inflows to sustain itself.

WHAT HAS CHANGED

So what could possible stop this ideal symbiotic relationship from continuing to feed on itself?

A number of factors, all of which are now coming together to end this Virtuous Cycle.

DEBT SATURATION

I recently authored a paper entitled Debt Saturation & Money Illusion , that if you have not read, I encourage you to read since it would take up too much space here. It makes the case that the global economy has reached the point where annual debt costs are now outstripping the global economy's ability to support the exponentially increasing burden.

Additionally, stimulus spending by governments has now reached the point where it is actually counterproductive.

The above chart shows that even using government numbers for inflation (which are disgracefully inadequate and understated) the real rates in the old industrialized economies are negative. By contrast, rates in emerging economies are positive.

This means central banks are effectively paying banks to take money, yet commercial banks cannot find sufficient investments to actually absorb the money. Like pushing on a string, the global economy simply cannot absorb debt at the levels required to sustain required growth rates which must exceed inflation rates.

The level of nonperforming bank assets is growing at such a rate that global banks have serious concerns with their existing loans and potentially their own solvency.

Growth in Non Performing Bank Loan Levels is shown below.

MALINVESTMENT

I found a recent article entitled: Technology firms struggle to cover interest payments in the Korean Times to be very instructive. Despite Asian economies growing rapidly and now dominating the global electronics industry, the study by the Korean Times found alarmingly that:

a. One in three firms traded on the Kosdaq stock exchange failed to earn sufficient money to cover their interest payments in 2010.

b. 280 out of 876 Kosdaq-listed corporations, or 32 percent, could not reach the benchmark reading of one in the interest coverage ratio. The interest coverage ratio, otherwise dubbed times interest earned (TIE), refers to the measure of a firm’s ability to honor its debt payments.

This is classic mal-investment in the truest sense of the Austrian School of Economcis.

Corporations now have balance sheets so leveraged with debt that their business models are barely able to cover debt payments even when interest rates are at historic lows. What does this suggest for possible debt default and forced unwinding going forward?

Private Equity corporations with leveraged takeovers and buyouts dominated the US financial landscape for years. These takeovers left corporate balance sheets severely damaged and barely able to pay the debt burdens they were forced to assume.

Additionally, we have learned since the days of Enron, there are significant amounts of debt held off balance sheets today in Special Purpose Entities (SPEs). There is no investor transparency to these obligations. This debt and other forms of 'contingent liability' reporting presently allow corporations to assume ever larger amounts of debt without impacting their corporate credit ratings. Everything works fine until growth slows.

Corporations over the last decade are acting more as highly leveraged hedge funds with the consequential exposure of margin or collateral calls. This is a highly risky and unstable situation in the longer term.

CONSUMPTION IMBALANCES

Another factor causing the unwind is a tapped out US consumer. This has been forecast for over a decade as an eventuality, but the US consumer continued to surprise everyone with their willingness to consume and take on debt. However, since the 2008 financial crisis things have changed. The US real disposable income has fallen and US consumer debt loads are now impacting their ability to consume.

Consumption growth rates in the US have slowed. The Asian economies have consumption rates below forty percent. The consumption growth rates of these Asian economies, though growing, are increasing from a much smaller absolute size. This imbalance is placing further pressures on the symbiotic relationship.

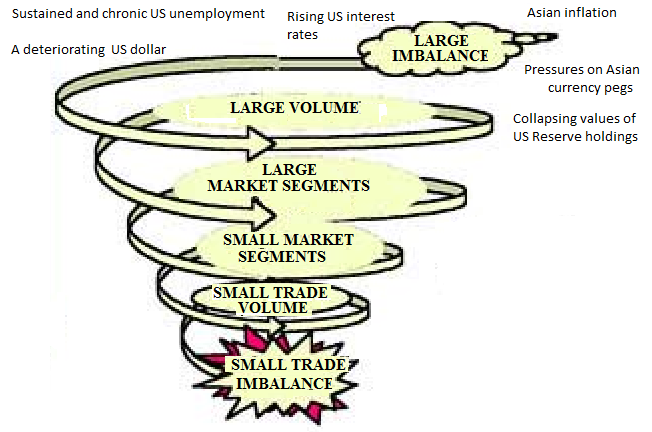

A VIRTUOUS RISING CYCLE BECOMES A VICIOUS DOWNWARD SPIRAL

Slowly, the cycle is reversing. What was once a virtuous cycle is now a potentially vicious downward spiral.

The death knell for the cycle will be:

1. A deteriorating US dollar,

2. Rising US interest rates,

3. Sustained and chronic US unemployment,

4. Asian inflation, especially in food where 60% of Asian disposable income is spent.

5. Pressures on Asian currency pegs

6. Collapsing values of US Reserve holdings.

BERNANKE'S BOX

I recently published another paper entitled BERNANKE'S QEx BOX! where I argued what Chairman Ben Bernanke was likely to do at his critical April 27th FOMC 'Signal' meeting. I was proven right as he delivered precisely on cue. It was not a difficult call.

http://www.zerohedge.com/article/guest-post-economic-death-spiral-has-been-triggered

May 27, 2011